Payment Gateway Integration

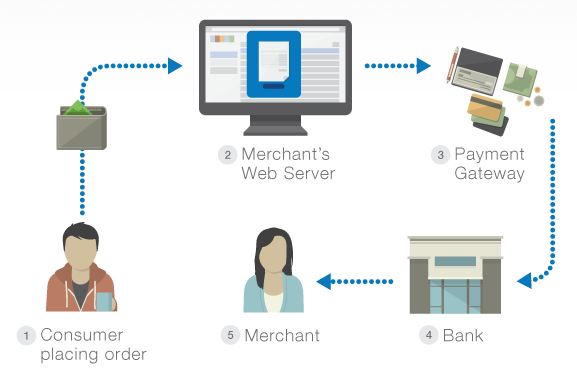

Today e-commerce sites accept credit cards as their primary form of payment. To accept credit cards, you need a merchant account with a bank. A payment gateway is simply a service which connects your Web site with the bank. While there’s a bit more to it than that, in essence that’s all it is – a way to take payments online.

Typically, when a customer enters credit card details on your Web site, those details are sent to the payment gateway, which then does some hard work in the background and processes (or rejects) the transaction. It then tells your shopping cart whether the payment was accepted or rejected. All this happens in a few seconds while the customer is waiting. The money is then transferred to your bank account – when that happens depends on the terms of your service.

There are three basic types of payment gateways. The first is an API (Application Programming Interface). This means that the customer never sees the payment gateway Web site – your shopping cart talks to it seamlessly in the background. This is generally the best option as it’s a transparent experience for the shopper, rather than being transferred to another site at the crucial moment of taking the money.

The second type is a third-party payment gateway. The customer starts the checkout process on your site, but completes payment on the payment gateway site. While this can be simpler to setup in some cases, the experience is unsettling for the customer, and you’ll probably lose a few sales. Some third-party payment gateways allow you to customize the page design

There are also integrated payment gateways. In this scenario, you don’t need a merchant account from your bank – the payment gateway does everything for you. For start-up businesses, this can be an easy start. Generally the fees are higher for an integrated service, but the trade-off is simplicity for the shop owner. The best known integrated gateways are PayPal and 2Checkout.